The fact there are leased EVs coming back and ending up in dealer lots in some number and so being less expensive by far than when they were new is indisputable.

According to the June “EV Market Monitor” from Cox Automotive, used EV sales are up 20.3% compared to what they were a year ago, undoubtedly reflecting the influx of vehicles.

And when it comes to pricing, the average listing price for a used EV in June was $38,342, which is actually up 7% compared to last year but still just $3,382 higher than a vehicle with an internal combustion engine—which listed at $34,960.

But looking at the new market, the average transaction price for an EV in June was $56,238 while the ATP for an ICE+ vehicle (the “+” signifies “hybrid”) was $49,558, or $6,680 less than the new EV.

So in the used space the EV is 9.7% more expensive but in the new space it is 13.5% more expensive than an ICE+ vehicle. And that is likely a price too far.

A data point for that is this: Director of Industry Insights for Cox Automotive Stephanie Valdez Streaty reports that the EV share of the new vehicle market in June was 5.4%.

One of the issues that consumers face in the new-car market in the U.S. is the non-trivial sticker price. According to Kelley Blue Book, the average transaction price for a new vehicle was $48,397 in September.

Charlie Chesbrough, Cox Automotive Senior Economist, said of the number, “One reason transaction prices are lower in 2024 is that many buyers are choosing smaller, less expensive vehicles. The subcompact and compact SUV segments are outperforming the market this year, and by no coincidence, they’re also two of the lowest-priced product segments in the market.”

Two points about that:

It is surprising to think that prices are “lower in 2024” when that number is above $48K.

Subcompact and compact SUVs are growing in popularity, but it seems the likes of GM and Ford are still more interested in the other end of the spectrum, which helps with their earnings now, but perhaps not for the long run, when people simply can no longer accept high monthly payments. (Given the number of large, expensive vehicles that are still being sold, it is clear many people continue to be accepting. But at some point other bills are going to take precedence. After all, when the average monthly car payment is on the order of $750, and the Bureau of Labor Statics found that car insurance premiums increased an average 20% between June 2023 and June 2024, something’s got to give.)

This phenomenon of going for the upper end of the market is not just one in the U.S.

Renault Rafale E-Tech 4×4 with the Atelier Alpine features a chassis and agility control system developed by the engineers of Alpine Cars. There is a self-adjusting ting smart suspension with a camera for predictive control. (Photo Clément Choulot / DPPI)

Renault just introduced a new plug-in hybrid crossover, the Rafale E-Tech 4×4. It is a 300-hp vehicle that has a 22-kWh battery that the company says can power the car some 105 km (65 miles) on the European WLTP schedule (which is different than the EPA).

What did Bruno Vanel, VP, Renault Brand, Product, Revenue & International Markets Expansion, say of the new vehicle represents? It “symbolizes our move upmarket and our legitimacy to conquer all customers with a high-performance version.”

When you think of European vehicles that are (1) upmarket and (2) high performance, odds are something from BMW comes to mind. And this is probably the case in France, as well.

But Renault wants some of those higher margins, too.

Most people need transportation but don’t necessarily want to compromise on how they achieve it but don’t want to be crushed by the sticker price. Enter the Jetta. . .

By Gary S. Vasilash

Cox Automotive’s “Auto Market Snapshot” for October 3, 2024, has it that the average used vehicle listing price was $25,172 (updated 9/20/24) and the average loan rate for a used car was 13.91%. And the average new vehicle listing price was $46,841 and the loan rate was 9.51%.

So taking those numbers into account, I am exceedingly impressed with the MSRP for the 2025 Volkswagen Jetta 1.5 SEL: $29,000. (Adding destination bumps it to $30,225).

Now were you to buy a used car at that average listing price of $25,172 and get a five-year loan fat the 13.91% rate (assuming nothing down) that vehicle would end up costing $34,929.

If you were to buy a brand-new 2025 Jetta for $30,225 and finance it for five years at 9.51% (again, assuming nothing down), you’d pay $38,320.

Or, a difference of $3,391 over the five-year period, or $678.20 per year.

Somehow it seems that ponying up $56.52 per month is well worth it for getting a car that is really quite impressive—and if you took at the average new vehicle listing price of $46,841, that $29K MSRP cannot be overlooked when the Jetta is a complete package.

2025 Volkswagen Jetta. (Image: VW)

When it comes to VW sedans, the compact Jetta is the proverbial last-man standing. The Passat, which the company once hoped would be its answer to the Toyota Camry and Honda According, went out of production in the U.S. after model year 2022.

Then there was the Arteon, model year 2024 was it in the U.S. for the upscale-but-affordable sedan.

This goes to the point that the U.S. is a tough market for sedans, especially when companies, including VW, are promoting their electric SUVs (the ID.4 in VW’s case), or their ICE SUVs (the Atlas, Atlas Cross Sport, Taos, and Tiguan, in VW’s case).

But apparently there are some people who recognize that the Jetta is a vehicle that fits their needs.

That is, in Q3 2024 in the U.S. there were 19,379 Jettas sold—making it the second best-selling vehicle in the VW lineup, with the Tiguan taking first place, at 21,231. This means the Jetta outsold the Atlas, Atlas Cross Sport, Taos, and ID.4.

Notably, compared with Q3 2023 the Jetta sales are up 35%, the biggest percentage increase of any of the VW vehicles.

This may go to the point of Cox’s findings about the high prices of vehicles nowadays.

The thing about the Jetta is that this is a completely competent vehicle, and that is not damning with faint praise.

The SEL is the top-of-the line Jetta. The S starts at $21,995, which is certainly something that plenty should consider (i.e., $3,177 less than that used vehicle).

But the SEL has much of the “stuff” that people want in a new vehicle—heated and cooled leather front seats (heated in the two back positions), a sunroof, 10.25-inch screen with navigation, BeatsAudio. . .

There is a 1.5-liter, turbocharged, direct-injection engine that provides 158-hp mated to an eight-speed automatic that offers both a sport mode and paddle shifting. The front-drive car is surprisingly peppy.

Adaptive cruise control, lane keeping assist, blind spot monitor. . .these and other tech-based features are part of the package.

The styling is more sophisticated than sporty or extreme: it is a design that won’t age fast.

It is sometimes said that kids swerve from the types of vehicles their parents owned.

So it went from sedans to minivans to SUVs. Perhaps we are getting to a point of a full circle.

The Jetta is certainly a good reason why that could be the case.

A few thoughts from the Cox Automotive Q3 assessment. . .

By Gary S. Vasilash

While new EV sales are growing—remember, this is from a small base, so the growth in total numbers is not all that impressive—used EV sales are really doing quite well, or so the numbers from Stephanie Valdez Streaty, director of Industry Insights, Cox Automotive, who has a keen focus on EVs, indicate.

That is, year over year there is an increase of 64.4% for used EVs while new ones year-over-year it is up 12.6%.

In August there was a 90-day supply of new EVs. There was a 38-day supply for used EVs.

Still Pricey

One likely reason for the increased used EV sales is that the average transaction price in August was $35,937, compared with $56,574 for new EVs.

Realize that the now-used EVs probably had an ATP north of $56,574 when purchased new, so the buyer of a used EV is undoubtedly getting quite a well-loaded vehicle for the money.

I wonder whether a second used buyer will be all that interested in a vehicle, given concerns about battery longevity.

Leases Matter

In the new EV market leasing continues strong, Valdez Streaty noted. At 39% she says it is almost double the industry average. This probably has something to do with the ability to get IRA tax credits for EVs assembled in the U.S. And luxury vehicles, of which there are still plenty with EV powertrains, tend to have more leases than mainstream vehicles, so it makes sense to lease.

Overall Numbers

Looking at the powertrains in vehicles in August, ICE vehicles are at 81.6%, EVs at 8%, hybrids at 8.5% and PHEVs at 1.9%.

If you think about it, as OEMs began to pour money into EVs they subtracted from hybrids (e.g., the Ford Explorer had been offered with a hybrid, but the ’25 model doesn’t have one).

The company that didn’t pull back on hybrids—which actually continued to expand its offerings—is Toyota. Valez Streaty says that in Q2 2024 Toyota had 47% market share for hybrids—more than twice Honda’s second-place 20%.

Ford, it is worth noting, came in third at 14%, undoubtedly thanks to the F-150 PowerBoost Hybrid model.

Hybrids are typically referred to as a “transitional technology.”

Seems that that transition is going to take a whole lot longer than those outside Toyota anticipated.

The European Union is ahead of the U.S. in the acceptance of electric vehicles. That is, according to Cox Automotive, in 2023 the EV share of the U.S. vehicle market was 7.6%.

The European Union has just reported that in 2023 the number of EVs registered represents 14.6%.

What’s interesting about the 2023 number in the U.S. is that Cox Automotive reckonings show that Tesla sales represented 55% of all EV sales in the U.S.

There are now 30 brands offering EVs in the U.S., including Tesla, yet the company that seems to be going out of favor through the first half of 2024 has 49.7% of the market.

Taking out its estimated (it doesn’t provide clarity about sales in particular countries, including the U.S.) 304,451 vehicles from the 2024 first half total of 599,372, that means there were a total of 294,921 EVs sold in the U.S. in the first half of 2024.

To put that into perspective, in the first half of 2024 there were 248,295 Toyota RAV4s sold in the U.S.

So this means that 29 vehicle brands sold 46,626 more vehicles than a single model.

Questions

It is easy to get excited about percentage increases until they are contextualized.

Will the number of EVs on offer continue to grow? Yes.

Will the number of EVs sold increase as they become available in different segments? Yes.

Will growth in EV sales continue should there be a change in Washington that eliminates the incentives to buy an EV?

There’s the question that doesn’t have an answer.

But there’s something that provides perhaps of a hint in Germany.

Cautionary tale?

Meanwhile, back in Europe, EV growth continues, primarily because of government support and/or regulations.

According to T&E, “Europe’s leading advocates for clean transport and energy,” during the first half of 2024 EV sales were up in the EU by 9.4%–but that’s by leaving out the largest car market, Germany.

With Germany, the EV sales grew in the EU by 1.3%.

The organization’s Lucien Mathieu, cars director, said, “Germany is the sick man of Europe when it comes to electric cars. Meanwhile, markets which have strong, predictable incentives for EV adoption are reaping the rewards.”

At the end of 2023 Germany stopped providing a subsidy for the purchase of an electric vehicle. T&E calculates that that caused a 16.4% decrease in EV sales in Germany in the first half of 2024.

According to T&E:

“In the first half of 2024, EV sales grew in markets with supportive regulatory environments:

In France, which has a social leasing scheme to provide cheap electric cars to low-income households, BEV sales increased by 14.9% in H1 2024;

In Italy, BEV sales increased by 7.0% in the first half of the year, with a sales peak in June 2024 when new EV incentives were launched;

In Belgium, the company car segment drove the BEV market with a 47.8% increase in the first half of the year;

In the UK, the ZEV mandate has driven the BEV market, with sales increasing by 9.2% in H1 2024.”

Which raises a question: are “markets which have strong, predictable incentives” real markets or artificial ones?

Germany has some appealing EVs from small VWs to generally lauded BMWs to Mercedes lux.

And it is not like no one is buying EVs in Germany: T&E has EV sales in the first half representing 12.5% of the market.

Still, given the amount of investment and attention paid to EVs, the numbers seem somewhat small.

When you think of the quintessential full-size pickup truck, the sort of thing that you imagine farmers loading with bales or hay or contractors carrying loads of gravel, it is probably the Ford F-Series.

With good reason, given Ford sells those trucks the way McDonald’s sells hamburgers. The numbers are staggering.

But odds are, those images of the F-Series are probably not entirely accurate.

BMW 5 Series. Or you could consider a pickup truck. (Image: BMW)

Listen to Erin Keating, executive analyst for Cox Automotive, talking about vehicle transaction prices in May.

First she notes: “The popularity of fully loaded, full-size pickup trucks that are more luxurious than many luxury vehicles is unique to the U.S. market.”

Which can be understood that (1) there aren’t a lot of full-size pickup trucks sold in other markets around the world* and (2) those trucks are probably used as utility vehicles (e.g., the opening examples).

Keating does on: “The Ford F-Series outsold BMW 2-to-1 in May, and BMW’s ATP [average transaction price] was only marginally higher than the F-Series.”

Whereas the average transaction price for a BMW in May was $72,946, the ATP for an F-Series was $67,837.

Now that’s about a five-grand difference, which isn’t exactly trivial.

But somehow a Bimmer seems as though it is in another category all together compared with something that you probably once saw with a decal of Calvin relieving himself on a Chevy bowtie on the back window of the truck.

Of course, not a $68,000 truck, but nonetheless. . . .

//

*That full-size pickups are pretty much indigenous to the U.S. market is something that makes the development of EV versions of the trucks somewhat problematic in the long run. That is, on a global basis something like the Ford Mustang Mach-E has more applicability than an F-150 Lightning. While it seems to have been thought by some OEM execs that because customers in the U.S. buy lots and lots of trucks, then if a somewhat sizable percentage of them buy electric versions then everything will be great. For reasons including cost and/or performance, that is not proving to be the case. This means that scale isn’t being achieved, and if there is something that is necessary for an OEM, it’s that. So by spending lots of engineering and manufacturing resources on making a type of vehicle that has a limited domestic market and a nearly non-existent global market, achieving scale is anywhere is not particularly likely.

Of the 100% of people who are planning to purchase a new or used vehicle in the next two years, Cox Automotive finds that 55% are “Considerers,” as in considering an electric vehicle and the remaining 45% are “Skeptics,” as in interested only in internal combustion engines.

From a demographic point of view, the Considerers are probably more appealing to dealers in that they have a higher average income than the Skeptics ($71,756 v. $60,625) and are younger (42 v. 46), which means they may have more vehicles in their future.

However, speaking of the future, Cox Automotive personnel expect that within the next three to five years 54% of the Skeptics will become Considerers, then an additional 26% in 10 years, meaning there will just be 20% remaining dedicated to combustion.

It is interesting to note that as for now, when it comes to barriers to EV adoption Considerers rank as 1 and 2 “Too expensive” and “Lack of charging stations,” while Skeptics flip the order of those two.

What is an interesting difference in barrier rankings is that for the Skeptics “Inability to charge EV at home” is in third place (tied with “Concern about battery losing charge”) while it is in fifth (or last) place for the Considerers.

Which presumably means home charging is acutely important for EV sales.

There are some potentially concerning numbers regarding the Considerers, however.

For example, in 2023 the EV Buyer was 41 years old, had an average household income of $139,00 and 84% of them had excellent/very good credit.

In 2024 the Considerer is 42, has an average household income of $72,000 and 53% of them have excellent/very good credit.

Still, according to Isabelle Helms, vice president of Research and Market Intelligence at Cox Automotive, “We remain bullish on the long-term future of EV sales in America, as many Skeptics today will be carefully considering an EV by the end of the decade. With more infrastructure, education, and technological innovation and improvements, we believe electric vehicle sales will continue to grow in the long term.”

One thinks about Keynes’ quote regarding the long run. . . .

Adjusting interest rates can be a tricky business for the Federal Reserve.

On the one hand, it wants to reduce the amount of borrowing and—consequently—spending.

That helps reduce inflation.

On the other hand, it doesn’t want to reduce the amount such that the economy falls into a recession.

Consumers don’t like inflation. That’s because things cost more.

Consumers don’t like high interest rates. That’s because they have to spend more to borrow the money to buy things.

Things like cars.

Kelley Blue Book announced the average transaction price (ATP) for new vehicles was down 1% in March compared to the ATP in February.

What’s more (or less), the March ATP was down 5.4% compared with December 2022, when ATPs were at their peak.

It’s not like new vehicles are inexpensive, even with that 1% drop.

The ATP—and remember, this is average—for March is $47,218.

Erin Keating, executive analyst at Cox Automotive, said, “It bears repeating that historically high interest rates and associated inflation combined with an ever-widening deficit of available vehicles at lower price points, will continue to challenge affordability for most car buyers.”

So there’s the interest rate-inflation situation.

The Disappearing Econo Box

Keating’s observation about “widening deficit of available vehicles at lower price points” is key.

KBB found that in March there were some 275 new-vehicle models available in the U.S.

Of the 275 only eight had ATPs of less than $25,000.

Three percent. Imagine trying to find one.

But apparently either people have lots of money or they’re willing to borrow it: in March sales of vehicles with ATPs above $75,000 were greater than those under $25,000: approximately 81,000 of the former and 52,000 of the latter.

Perhaps high interest rates are having an effect—on the lower portion of the market.

Of course, chances are OEMs are putting out vehicles with higher sticker prices because they can make more money on them than those that are more economical.

U.S. dealers are not particularly keen on electric vehicles (EVs).

So indicates the Cox Automotive Dealer Sentiment Index (CADSI) released this year.

When asked how EV sales were doing in Q1, the index score was 42. That’s off from 50 in Q1 in 2023.

And while 42 may not be particularly meaningful, know that it is the lowest score since the question was included in CADSI in Q2 2021.

The outlook among dealers regarding EV sales going forward isn’t good, either.

In Q1 2023 the index score was 53. Back then, a majority of dealers saw EV sales growing.

In Q1 2024 that index score is down to 36.

That’s the lowest score for EV outlook since that question was asked.

Seems things are no longer anticipated to be growing for EVs.

It seems as though this is not simply a U.S. phenomenon, either.

While Cox was looking at new vehicle sales, over in the U.K. and outfit that specializes in used vehicles—going from consumers to dealers rather than the more conventional vice-versa—found that sales are not particularly robust.

Compared with last year, HonkHonk found 38.5% of dealers are “much less interested” in EVs and 12.3% are “a bit less interested.”

Or 50.8% of dealers are not all that keen on putting EVs in stock.

Sebastien Duval, CEO of HonkHonk, said, “Right now, dealers can’t get enough small or medium petrol cars, medium diesels and even hybrids, since the market began recovering in 2024. But less than one in ten of them want to snap up a battery EV car more than they did than a year ago.”

That’s right: Diesels are more appealing than EVs in the U.K. used market.

During his “Forecast: 2024” webcast presentation, Jonathan Smoke, Cox Automotive chief economist, made a number of observations and predictions that ought to make potential vehicle purchasers happy.

Like the likelihood that the unemployment rate will stay at 4.0-4.1% throughout the year; that inflation will slowly decline; that interest rates will go in the right direction for those who need a loan.

Charlie Chesbrough, Cox senior economist, pointed out that new vehicle inventory in 2023 was up 51% compared with 2022, and one consequence is that incentives are rising, so it appears that there is going to be a shift from a seller’s market to a buyer’s market.

And speaking of buyer’s market and inventories: Stephanie Valdez Streaty, Cox director of Industry Insights, noted that at the end of 2023 the day’s supply of ICE vehicles on dealer lots was 69 days—but it was 113 days for electric vehicles. There is likely to be some dealing.

But there was one point that Smoke made that shows just how important vehicles and costs associated with them are to people.

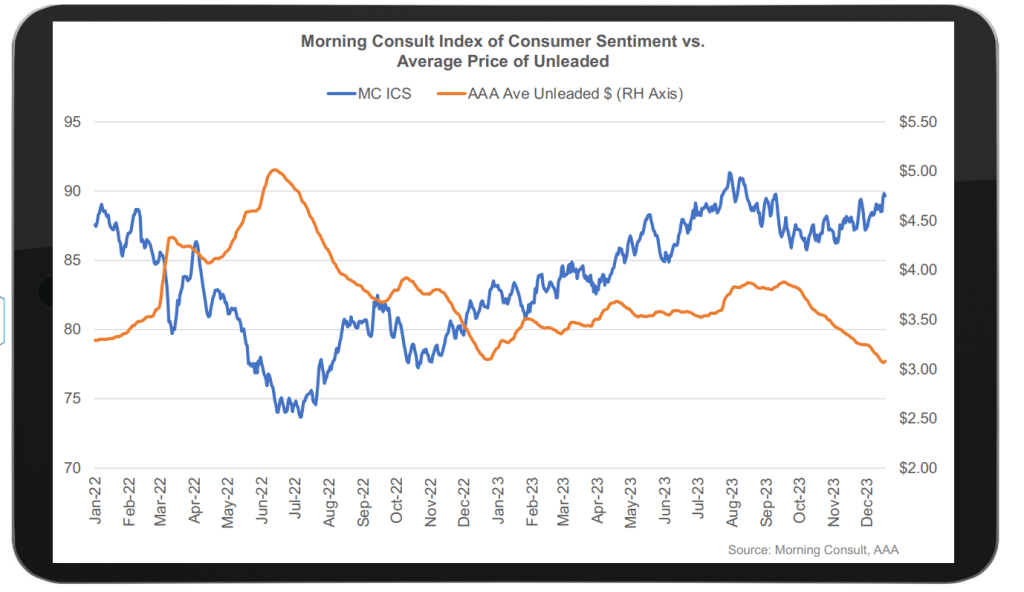

As the graph below shows, as the price of gasoline goes down, the state of consumer sentiment rises.